New Construction Investing: Contracts, Pricing, Risks, and Cash Flow Math (A Playbook for Your First Deal)

Learn about New Construction for real estate investing.

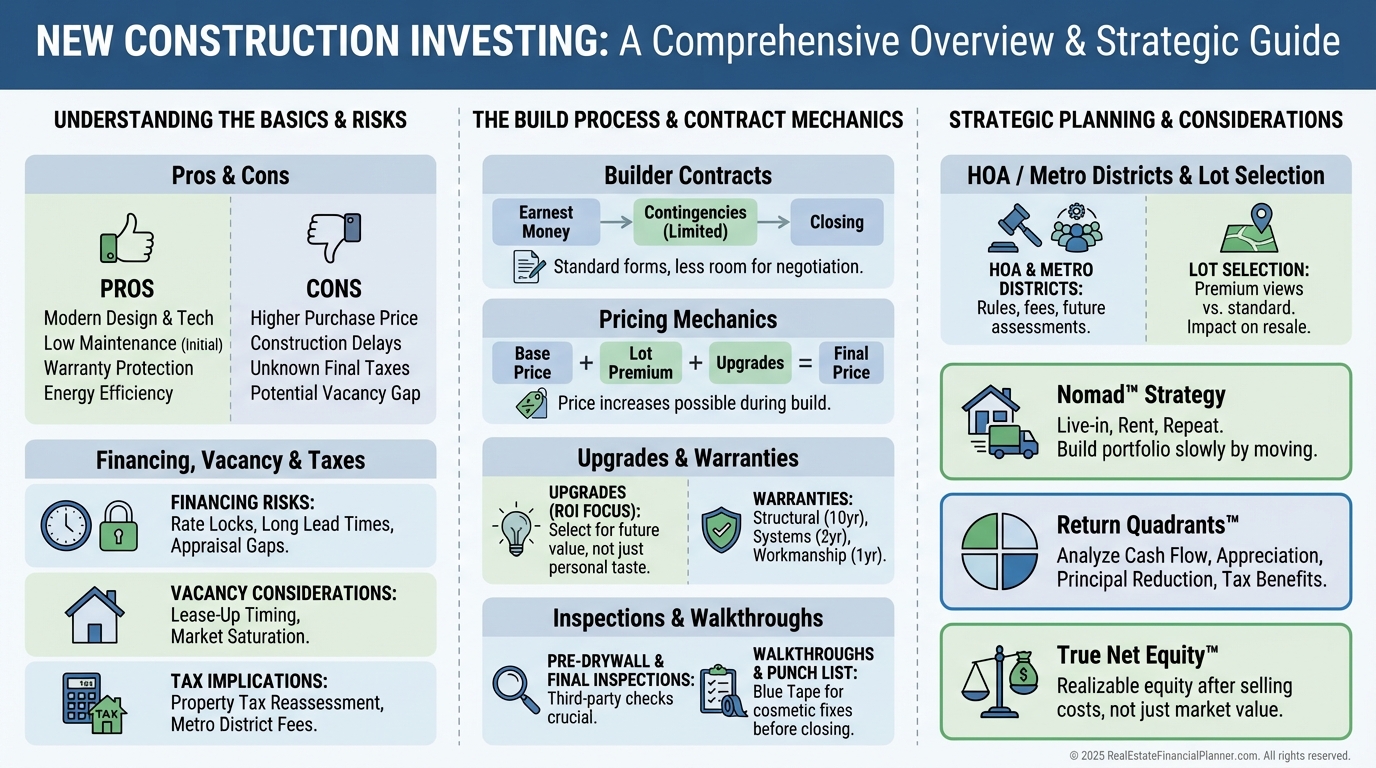

Why New Construction For Your First Investment

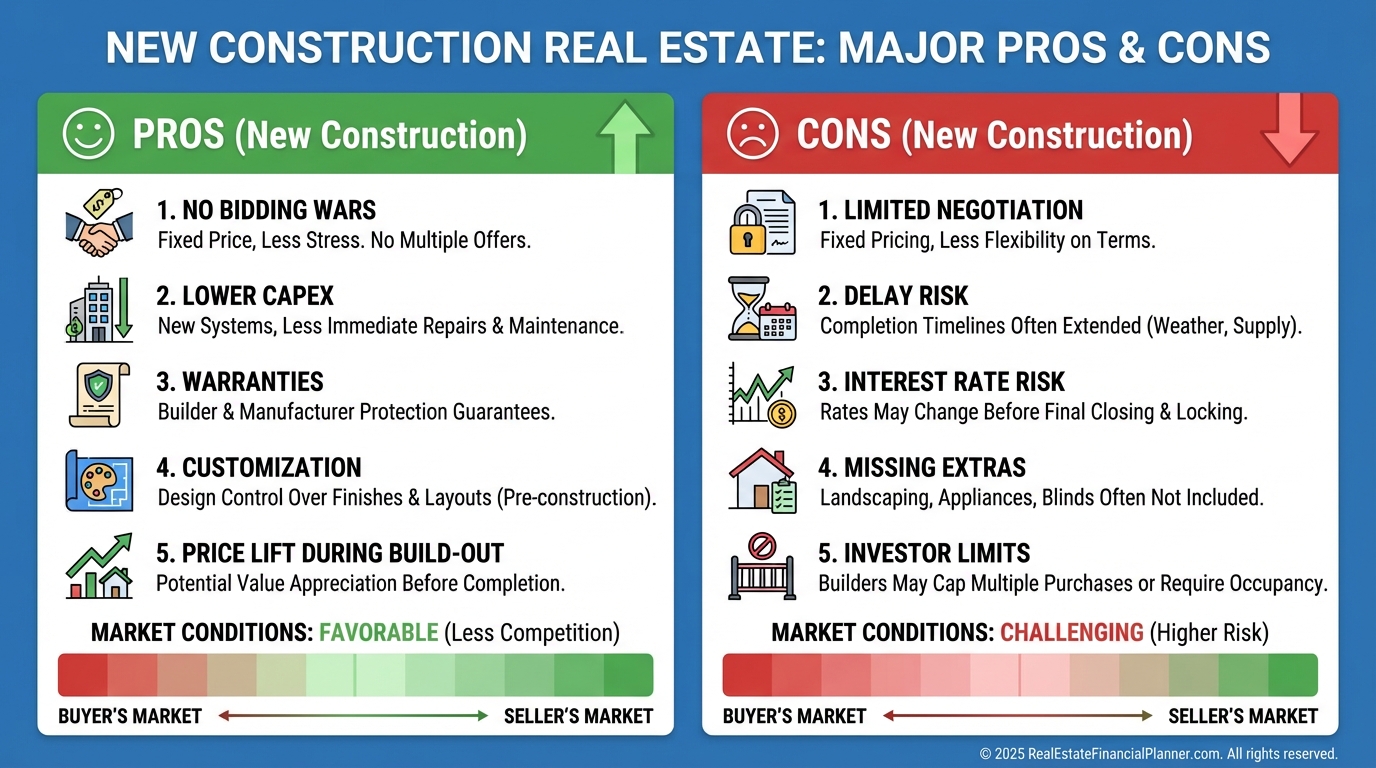

When I help clients buy their first rental, new construction often wins because it front-loads reliability and reduces surprises.

You trade some purchase price premium for lower near-term CapEx, modern tenant-pleasing finishes, and builder warranties.

In strong markets, I’ve watched clients “walk into” equity as builders raise prices during the subdivision build-out.

In soft markets, I’ve coached clients to capture incentives or standing inventory discounts instead.

Your edge is knowing when you’re in which market and modeling outcomes before you commit.

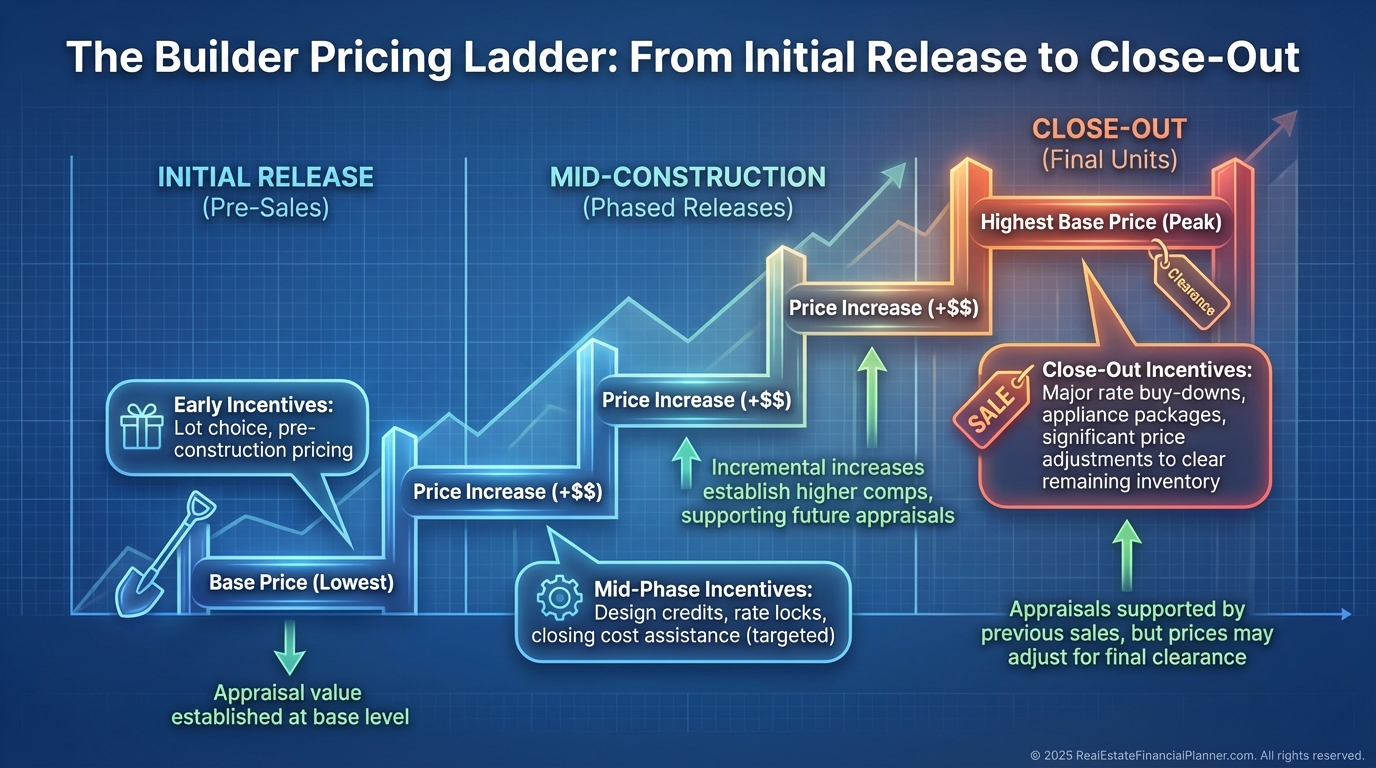

How Builders Price (And How Investors Profit)

Builders typically release homes at a base price, then notch prices up as contracts accumulate.

Those higher comps support later appraisals and keep the price ladder rising through the phase.

Incentives rotate to create urgency—one weekend it’s free A/C, another it’s closing cost credits or rate buydowns.

Buy early to ride builder price lifts, or buy late to capture close-out discounts on less ideal lots.

Model both paths in the World’s Greatest Real Estate Deal Analysis Spreadsheet™ and compare outcomes with Return Quadrants™ over 1, 3, and 5 years.

Contracts, Representation, and Leverage

Most builder contracts are attorney-drafted to protect the builder and place timelines and remedies in their favor.

Earnest money often goes “hard” early—especially after design selections or change orders—so know precisely when funds become non-refundable.

The builder’s sales rep represents the builder, not you.

Bring your own agent, and when terms are unclear or high-dollar, have your attorney review the contract.

I also ask for the contract early and highlight red-flag clauses for clients: assignment limits, termination rights, completion flexibility, and post-closing punch list handling.

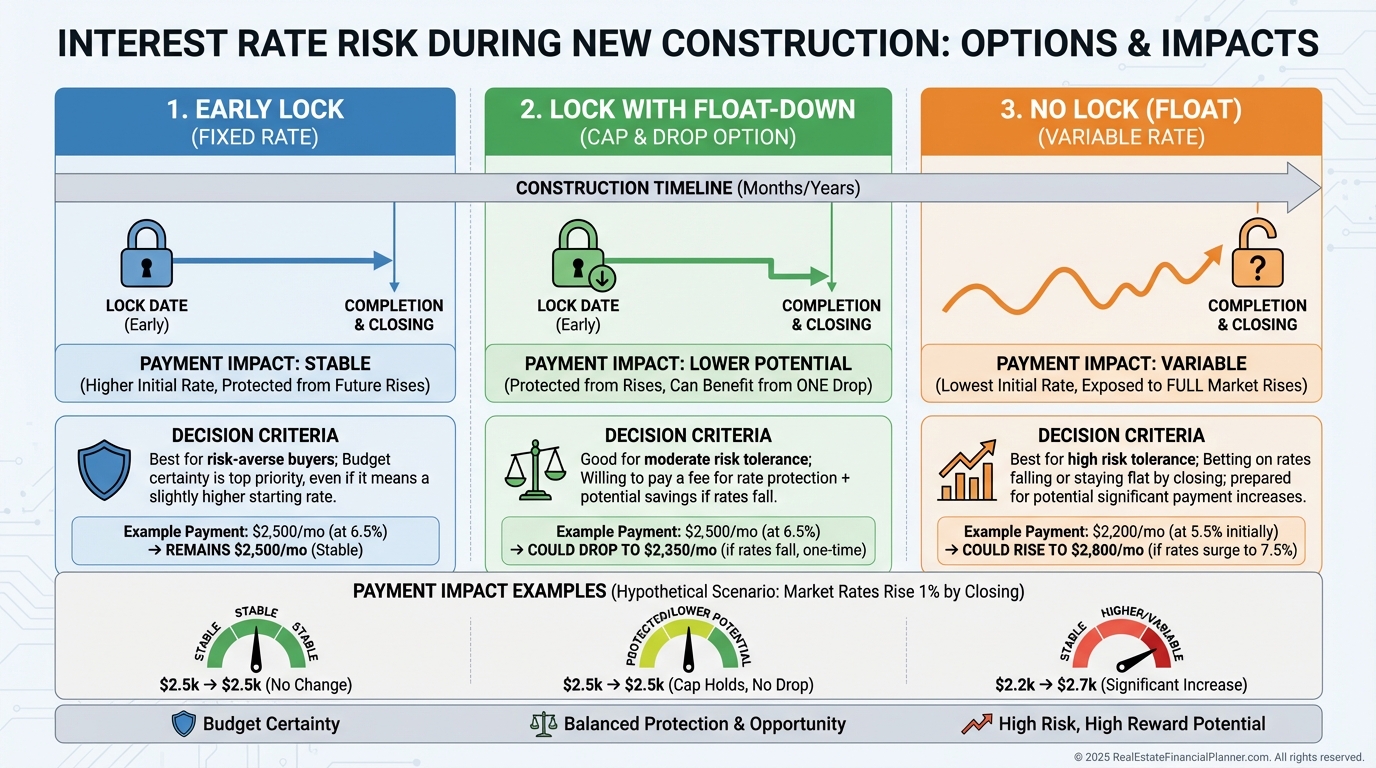

Financing Risks, Rate Strategy, and Preferred Lenders

The biggest new construction risk I manage for clients is interest rate movement between contract and completion.

If we can lock early with a float-down option, we price the lock cost versus worst-case payment risk and decide.

Builder-preferred lenders can be cheaper after incentives like rate buydowns or closing credits, but I still compare them to outside lenders.

For appraisals, budget more than resale, because appraisers may do multiple site visits and final inspections.

Always track seller concessions so they aren’t lost to lender caps or misapplied credits.

Cash Flow Focus: Price Point, Math, and Return Quadrants™

Cash flow usually looks best on lower-priced models in the same community.

Then I overlay Return Quadrants™ to see the full picture: Cash Flow, Appreciation, Principal Paydown, and Cash Flow from Depreciation.

Finally, I calculate True Net Equity™ to account for transaction costs and loan payoff so clients know their real, spendable equity.

If it only works because of rosy rent or tax assumptions, we pass.

What Builders Include (And Why It Matters)

Different builders have very different standards that change your maintenance and rentability profile.

Flooring, countertops, trim, fixture quality, doors, backsplash, appliance packages, and energy features vary widely.

Durable, in-style, easy-to-replace finishes often reduce long-run turns and maintenance.

I’ll often prefer luxury vinyl plank over sheet vinyl, entry-level stainless over mismatched white, and quartz over laminate when the rent spread or reduced turnover supports it.

Garage count, backyard landscaping, and patios influence demand and vacancy, especially in family-oriented submarkets.

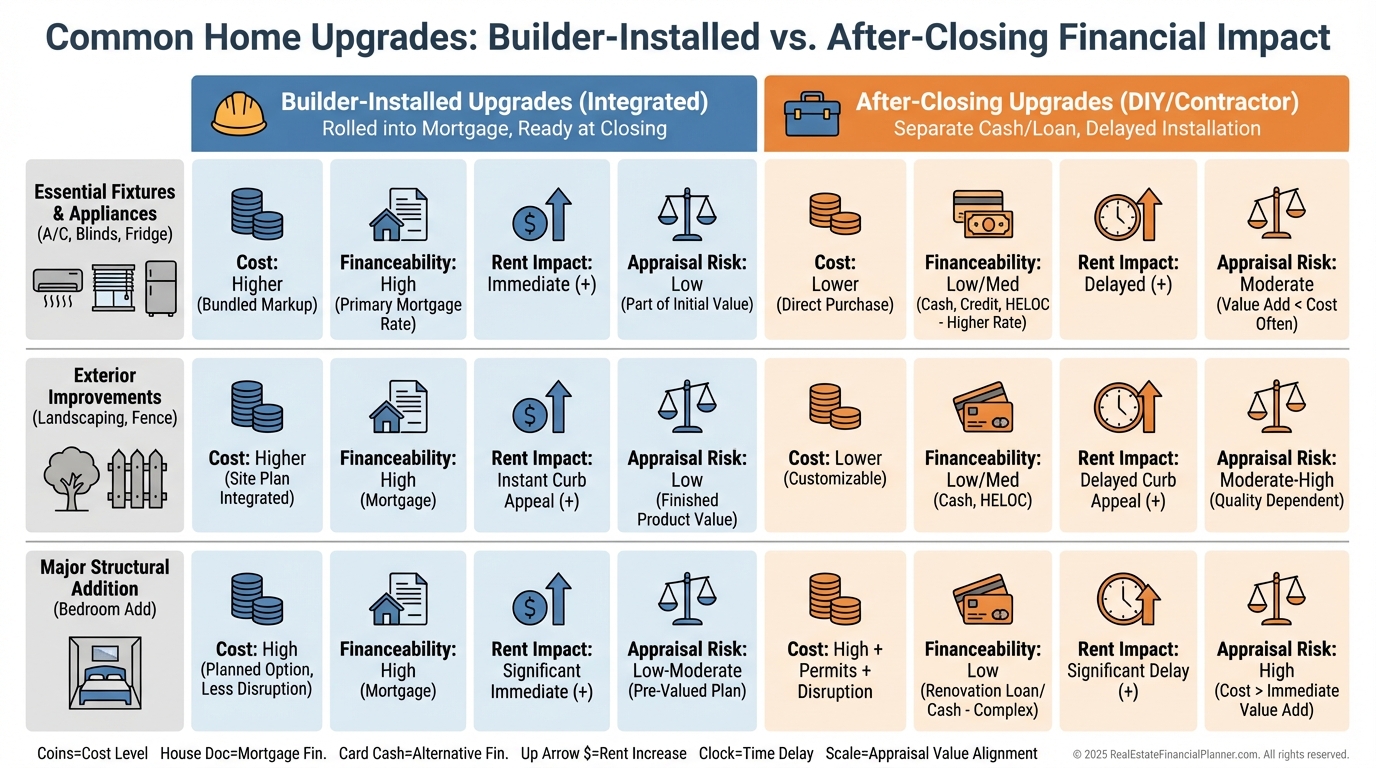

Upgrades: What To Buy, What To Skip, and Bedroom Math

Upgrades priced into the loan improve cash-on-cash returns by lowering your cash outlay, even if the line-item is costlier than buying after closing.

I price each upgrade two ways: financed vs. cash after closing, then estimate rent impact and time-to-rent benefits.

Air conditioning, basic blinds, fridge, and garage door opener are frequent “buy with builder” items for convenience and financeability.

Fencing and backyard landscaping are case-by-case depending on neighbors, HOA rules, and whether I can cost-share later.

Converting a loft to a bedroom might add roughly $10K, which could be $50/month in payment; if rent rises by more than that and vacancy falls, I greenlight it.

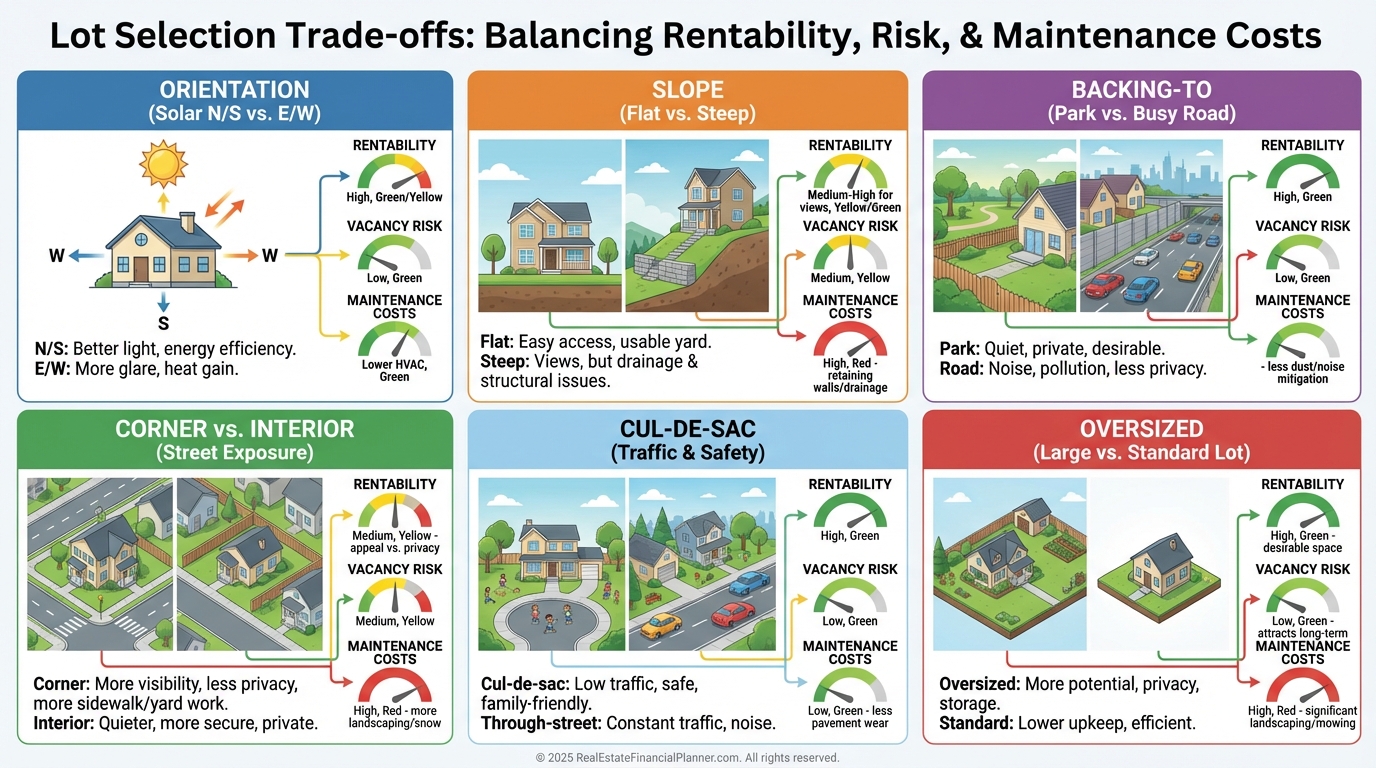

Lot Selection That Rents Fast (And Ages Well)

Lot premiums can be worth it if they create outsized demand or resale lift.

I watch driveway orientation in snowy markets, slopes that imply retaining walls or drainage fixes, and what the property backs to.

Corner lots can mean more shoveling and exposure, but some tenants love the extra parking and no side neighbor.

Cul-de-sacs are quieter but can have odd yard shapes and limited parking.

Oversized lots cost more to fence and maintain and rarely pay back in rent unless you’re in a yard-hungry submarket.

Builder, HOA, and Investor Limits

Some builders cap investor sales or prohibit them during early phases.

HOAs may limit rentals, ban STRs, or cap rental percentages.

If we’re using Nomad™, buying as an owner-occupant and converting later often navigates those limits better, but we still read the docs line by line.

And I warn clients that HOAs can vote to add restrictions after purchase, so plan for that tail risk.

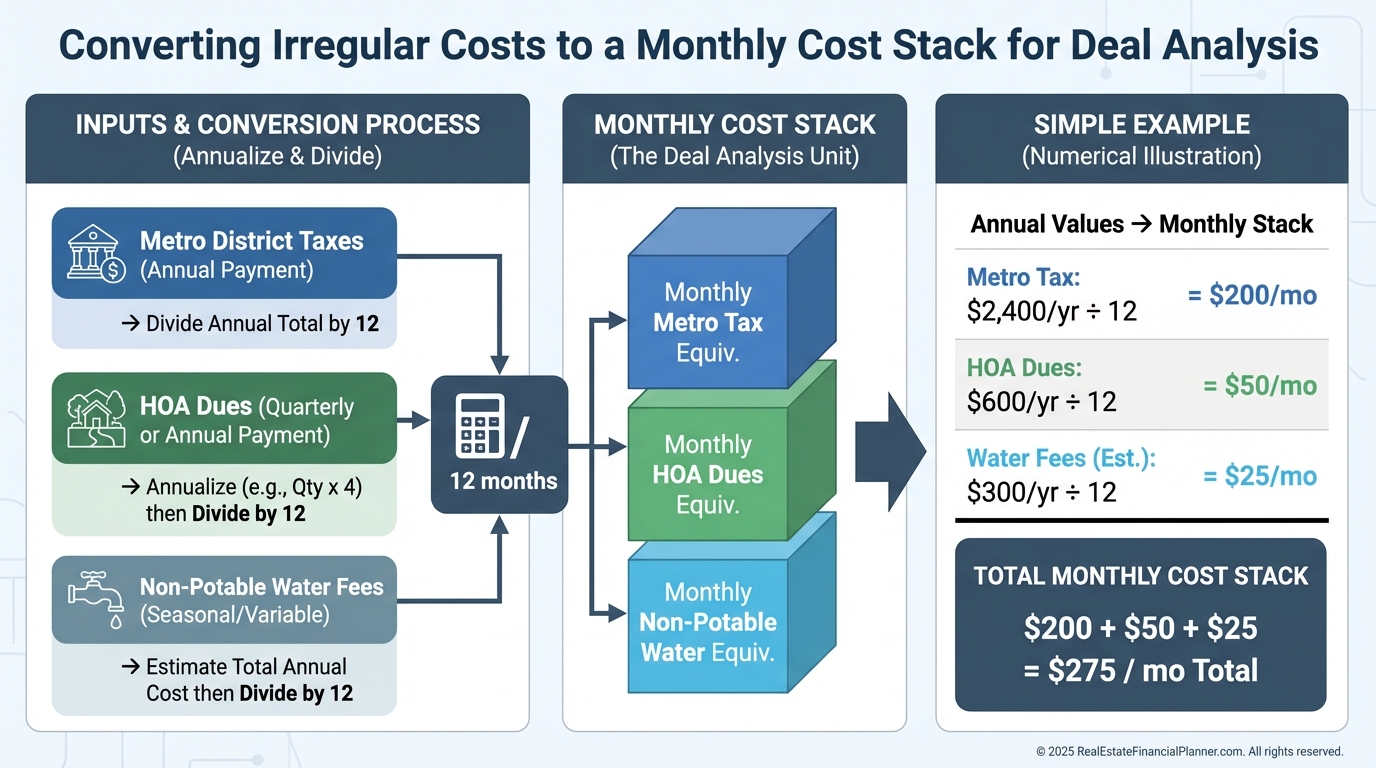

Metro Districts, Non-Potable Water, and Your Real Monthly

Metro taxing districts fund infrastructure, which can keep base prices lower but raise your annual tax.

Sometimes you’ll pay both metro and an HOA.

Non-potable irrigation water might be included in the metro fee or billed separately, and I try to pass that through to the tenant when leases allow.

I always convert annual taxes, metro, HOA, and utility line items to monthly and model them explicitly.

Vacancy, Access, and Marketing in a Construction Zone

Builders often restrict access before closing, which limits showings.

In investor-heavy phases, many near-identical rentals can hit the market at once.

I start marketing early with floor plans, builder photos (with permission), and sample unit photos, then pivot to professional photos as soon as we close.

Nomad™ helps avoid the initial flood because you rent a year later when the neighborhood is quieter and supply has normalized.

Inspections, Walkthroughs, and Warranty Timing

Municipal inspections check code, not investor-grade quality.

I like a pre-close inspection for punch list context and a second inspection around month 10–11 for warranty claims.

Do a thorough blue tape walkthrough knowing not everything will be done by closing.

Use the builder’s warranty portal and submit clear photos and descriptions, then calendar follow-ups.

Sewer scopes catch construction debris or install errors, and radon tests confirm whether a passive system needs to be activated.

Small concrete cracks are normal; heaving is not—document and claim before the warranty clock runs out.

Site Visits, Safety, and the PITA Clause

Most contracts limit jobsite visits without permission for safety.

I schedule escorted visits and avoid directing subs or requesting ad hoc changes.

Some contracts include a “PITA” termination option if buyers disrupt construction.

Be involved, not intrusive.

Photos and Launch Plan

I book professional photos the day we close, even if landscaping isn’t finished.

We shoot the clean, vacant interior first and update exterior shots when fencing or sod is complete.

Crisp photos shorten time-on-market and pay for themselves quickly.

Property Tax Delays: First-Year Boost, Then Normalize

Your first-year taxes might reflect land or partial completion.

I call the assessor to learn the exact local rule and never underwrite the deal assuming a tax delay.

When the full assessment hits, the property still needs to pencil, so I underwrite with stabilized taxes and treat any delay as a bonus.

Extended Warranties: Cheap Sleep

Third-party new construction warranties can extend coverage well beyond the builder’s term.

The service-call model caps your per-incident outlay and improves expense predictability.

I skim the exclusions and compare cost versus expected failure rates in years 2–5.

Fencing Strategy

If builder financing allows, I’ll sometimes include fencing in the mortgage when rentability demands it.

Otherwise, I’ll wait, coordinate with neighbors, and split costs where allowed.

HOA fence rules can change your price and timeline, so I verify specs up front.

Agent Or No Agent

I have not seen reliable builder discounts for unrepresented buyers.

Builders budget commissions into pricing and value agent traffic.

Your agent advocates for you while the builder rep advocates for the builder.

Speculation and Lease-Option Variants

Pure speculation—contract now, resell the paper or flip at CO—can work in fast markets but carries real earnest money and market risk.

Most builder contracts limit assignment and discourage quick resales.

An alternative is lease-option: lock pricing early, place a tenant-buyer, collect option consideration, and ride builder price lifts.

It’s still risk-bearing, so I only pursue it when the math survives conservative assumptions and the exit is legal and permitted.